How to Make the Most of Your Savings

“Don’t save what is left after spending, spend what is left after saving,” says Warren Buffet.

Some of the world’s wealthiest contribute their success to their innate frugality. Even with billions of dollars in the bank, they live well beyond their means. This is not an exclusive club, of course. Everybody can teach themselves to become thrifty with practice.

Just saving money isn’t enough, though. Cash sitting in the bank account collecting dust fetches the account holder meager returns. Savings can be deployed to earn superior returns. The key is to start early to make the most of your savings.

4 Ways to optimally deploy your savings

The sooner a person begins to save, the more they will be able to amplify their wealth. There are several smart money moves an individual can make to grow their savings.

However, different people have different risk appetites and therefore require a different strategy. Let’s walk through a couple of ways that can help an individual make the most of their savings.

Start investing early

Compounding indeed is the eighth wonder of the world. The more time investments have to grow, the more exponential their growth will be.

Investing isn’t as simple as depositing money into the savings account, primarily because of the risk associated with different asset classes. All asset classes vary greatly in terms of risk and return. As a rule of thumb, Finance 101 states that higher the risk, higher the return.

This makes sense, doesn’t it? Why would someone be willing to take on more risk if another asset class with a lower associated risk offers similar returns?

That leads people to the next question; where should they invest? Well, where a person should invest depends on their time horizon, risk appetite, and overall portfolio. While it’s non-negotiable to work with a financial advisor for professional guidance, let’s talk about some basics.

Savings can be categorized as either an unallocated surplus, emergency fund, or money dedicated to a certain goal. Savings that are set aside as an emergency fund or dedicated for short-term goals should be invested in a risk-free asset such as a certificate of deposit.

On the contrary, surpluses and savings dedicated to moderate to long-term goals may be invested in asset classes that can provide growth. Undeniably, these assets come with their fair share of risk. Someone who can’t afford to lose this capital, shouldn’t invest in these assets.

Cryptocurrencies are quite the buzz right now, and for all the right reasons. They offer massive return potential but can be frighteningly risky too. However, there is some middle ground for risk-averse investors interested in cryptocurrencies.

For instance, look at the following charts for a comparison between Bitcoin and Tether (USDT).

BTC:

USDT:

Notice how USDT is not nearly as volatile as BTC. Over the last 3 months, USDT’s largest drop was about 4 cents, while BTC dropped over $15,000. That’s huge, to say the least.

Stablecoins are a group of cryptocurrencies, the value of which is pegged to a fiat currency. They tend to be far less volatile than other cryptocurrencies like Bitcoin or ETH. Investors interested in stablecoins can buy Tether (USDT) since it has been the best-performing stablecoin thus far and is pegged to a strong fiat currency.

Alternatively, equities are a great option too. They continue to outperform almost any other traditional asset class. For investors that can’t actively manage their investments, mutual funds and ETFs should be a go-to choice.

Get comfortable with spreadsheets and budgets

Budgeting is a powerful tool when it comes to personal finance. Not only does it track where each dollar is being spent, but also uncovers potential loopholes in a person’s financial strategy.

It’s only when a budget is prepared that some realize that they spend $300 a month at Starbucks. This is why preparing a monthly budget and recording each month’s expenses to compare with the budget at the end of the month can be helpful. Take note of the deviations and be sure to eliminate them the following month.

Next, take things up a notch. Factor in a fixed amount of investment for each month – don’t shy away from being aggressive here. Allocate the monthly income to investment, retirement fund, and other goals. Spend what’s left on lifestyle expenses, but it’s completely fine (and actually preferable) to put that surplus away if anything is left of it.

For the first few weeks, the cash crunch may cause some real pain. However, it will start to get easier with time as those savings build up in the bank and your statements begin to show a consistent 4 or 5-digit figure instead of the usual few hundred dollars.

Budgets help fence your scope of spending and provide a clear cadence for investments. This inculcates discipline and cultivates financial prudence. Over a longer time frame, these factors can make a person’s financial position amply strong.

Chase the debt away

Think of debt as metaphorical shackles that hold people from achieving their financial freedom. The longer the debt remains outstanding, the more interest it accrues. The interest a borrower pays each month could have otherwise been a potential investment that could have earned a return.

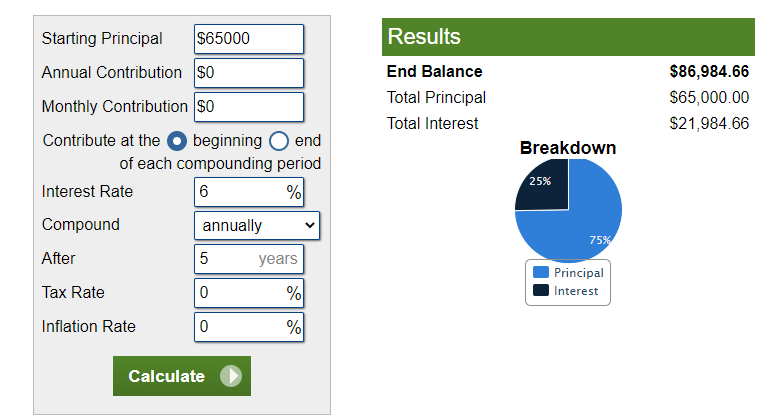

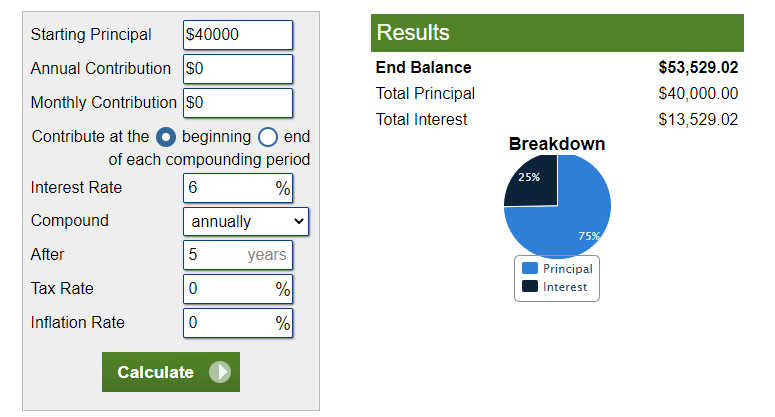

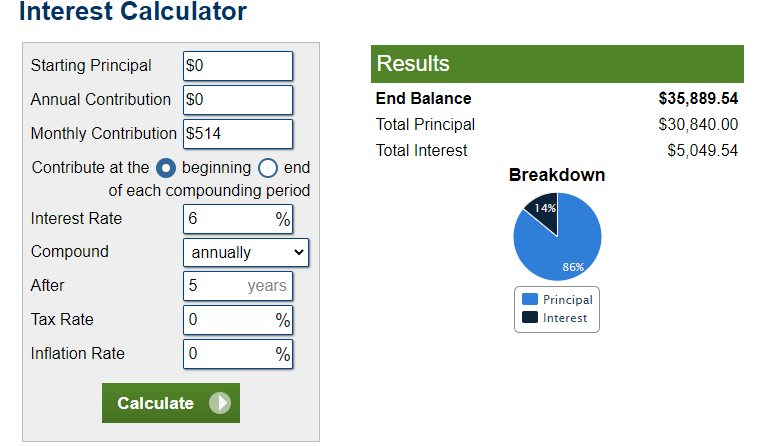

Let’s crunch some numbers to add context to this argument. Assume that a person has $75,000 in savings and $25,000 outstanding on their student loan. The first $10,000 is to be kept as cash to maintain liquidity, but the remaining $65,000 is treated as investible.

The person has considered investing the $65,000 in a certificate of deposit that will yield 6% per annum for 5 years. However, the student loan accrues interest at the rate of 9%.

The interest rate itself suggests why paying off the $25,000 loan should be prioritized over the CD investment. What’s more, the amounts being paid towards the loan repayment could also have otherwise been invested each month.

Let’s look at how much of a difference it makes in dollar terms.

Following are the charts depicting interest earned/paid on

- investment of $65,000

- Investment of $40,000

- Interest expense on $25,000

- Monthly investments of $514 (i.e., payments currently being made towards the student loan)

Interest earned on $65,0000:

Interested earned on $40,000:

Interest paid on $25,000:

Therefore, the payoff under each scenario:

- Investing $65,000: $21,984 (Interest earned) – $5,882 (Interest Paid) = $16,102

- Investing $40,000 after paying off the student loan and earning interest on monthly investment of $514: $13,529 + $5,049 = $18,578

The difference between the two payoffs widens even further over a longer time frame or when compared with high-return asset classes like equities instead of a CD. Plus, it’s also possible for student loan rates to be considerably above 9%. Therefore, always consider paying off debt before investing the savings.

High-Yield Savings Account

Everybody needs some level of liquidity. It’s unwise to invest all of the savings in long-term assets, including a CD.

Sure, CDs are safe and offer greater returns. However, they can’t be liquidated without being imposed a hefty penalty. Other assets like equities are highly liquid, but they are risky, and redeeming them for an emergency may sometimes involve erosion of capital.

The best option to keep the funds liquid is a savings bank account. There is just one issue, though. Savings accounts offer an extremely low annual percentage yield (APY).

To get around this, it’s worthwhile to approach the bank with which a person has their checking account opened already. Often, banks offer deals if a customer with a checking account also maintains their savings account with them. The deal is generally in the form of a waiver for the monthly checking account fee.

That being said, there are several other options outside of a person’s existing bank too. A common reason why some people may not be keen on opening a savings account with their existing bank is because of low yields.

While putting money in an FDIC-insured savings account with the current bank will offer safety and liquidity, it has a trade-off; the low APYs. For earning better yields, consider setting up an online savings account.

While the difference between both APYs will generally be less than one percent, the money will still be safe and earn a relatively higher rate of return. The sole aim here is to maximize return while holding the risk and liquidity constant.

Feel confident about making the most of your savings?

Saving is half the battle won. To make the most of your savings, they need to be planted so they grow and generate passive income. The tips discussed above will provide an insight into how individuals can put their savings to use most effectively.

Just letting the entire savings sit in a savings account is inefficient; there is much more return potential to be leveraged by investing this money. While it wouldn’t be smart to invest all of it, creating a well-balanced portfolio of diverse assets can maximize returns on savings and fast-track the process of long-term wealth creation.